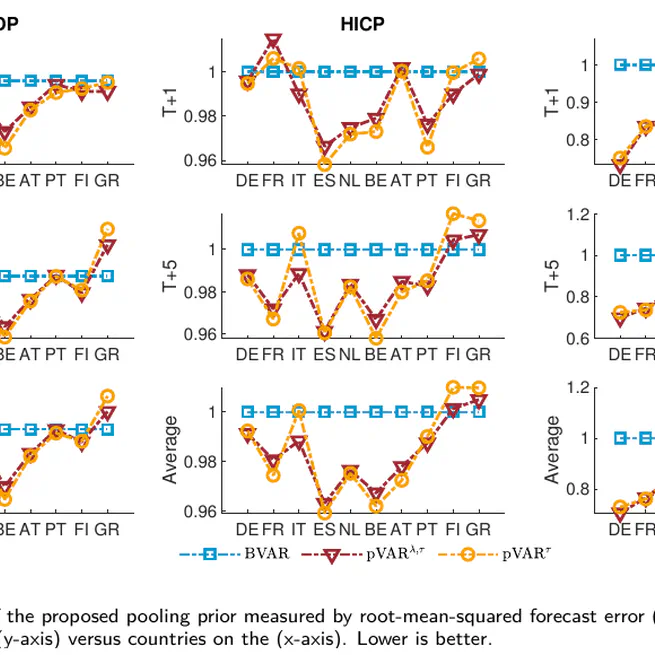

Improving inference and forecasting in VAR models using cross-sectional information

We propose a flexible prior for vectorautoregressions (VARs) which can exploit the panel structure of macroeconomic time series and at the same time provide shrinkage towards zero in order to address overfitting concerns. The prior is flexible as it allows for parameter pooling across both a country dimension (two countries are completely alike) and/or variable dimension (dynamics of two variables across countries are alike). The usefulness of our approach is demonstrated via a Monte Carlo study and an empirical application using a large euro area data set. We find that cross country information helps deliver sharper parameter inference that improves point and density forecasts as well as structural analysis through lower estimation uncertainty. Also it is beneficial to have both pooling and shrinkage instead of only pooling.

Jun 1, 2022

The investment narrative: Improving private investment forecasts with media data

In this paper we use newspaper articles to generate time series that are related to corporate investment and look at their ability to predict its dynamics.

Dec 13, 2021

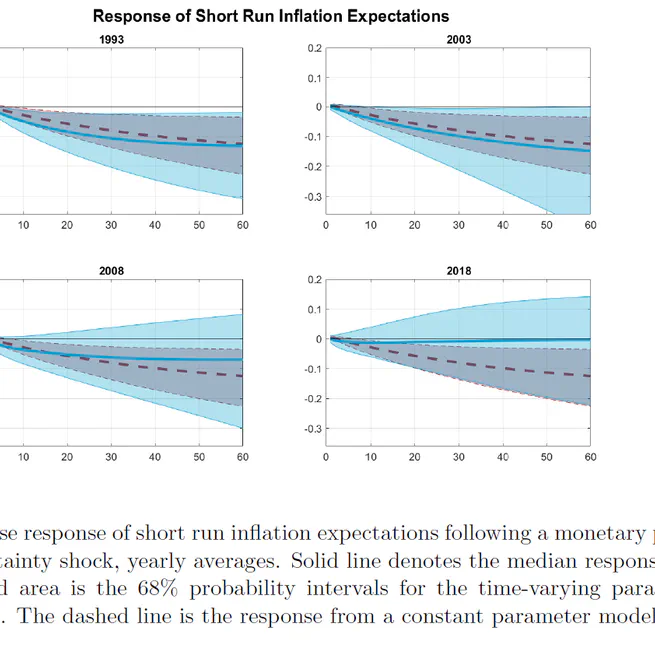

Monetary policy uncertainty and inflation expectations

In this paper we study whether inflation expectations in the U.S. react to changes in monetary policy uncertainty (MPU) as measured through the volatility of monetary policy shocks. We find that while they did, the importance of MPU has diminished and that it has different effects on short versus long-term inflation expectations.

Mar 1, 2021