Economic Knock-On Effects of Russia’s Geopolitical Risk on Advanced Economies: A Global VAR Approach

Oct 1, 2024

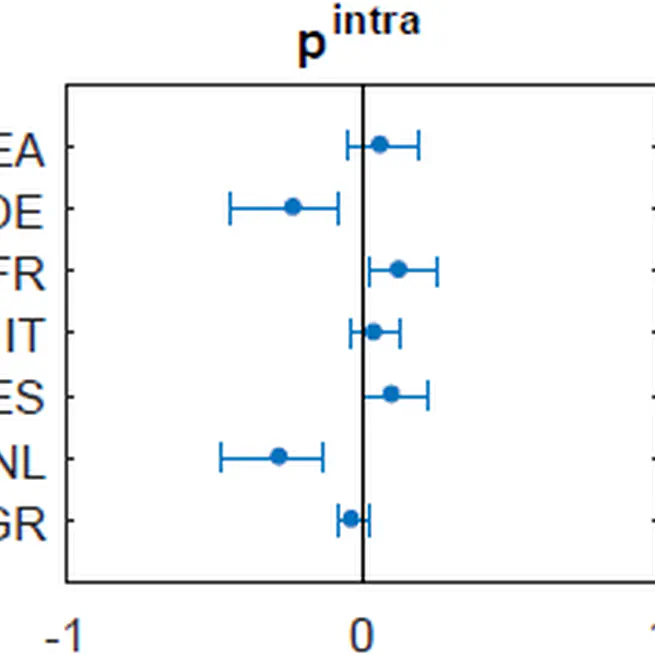

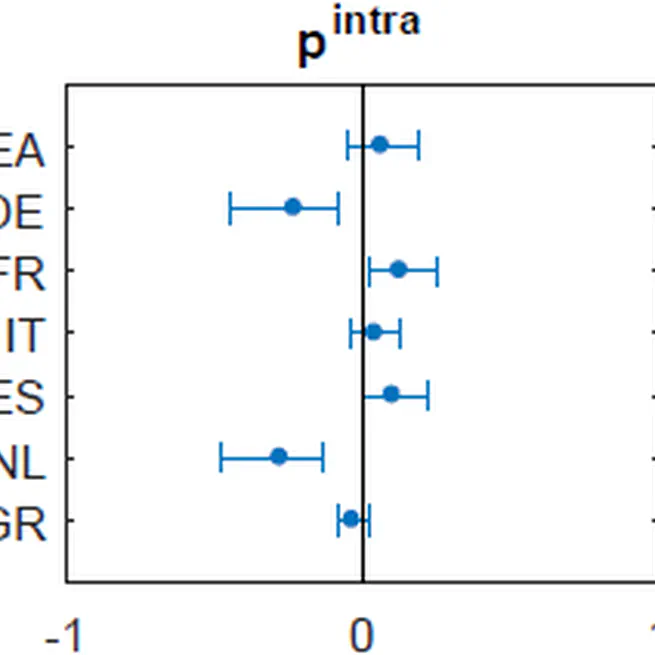

Exchange rate uncertainty and import prices in the euro area

This paper analyses the effects of exchange rate uncertainty on the pricing behaviour of import firms in the euro area. Uncertainty is measured via the volatility of the structural shocks to the exchange rate in a non-linear VAR framework and is an important determinant of import prices. An increase in exchange rate uncertainty is associated with a fall in prices on average, which suggests that the exchange rate risk is borne by the importers. The analysis utilizes a dataset on industrial import prices, disaggregated by origin of imports. Controlling for intra- and extra-euro area trade is important.

Aug 16, 2019

Financial crises and time-varying risk premia in a small open economy: a Markov-switching DSGE model for Estonia

May 2, 2018

The credibility of Hong Kong's currency board system: looking through the prism of MS‐VAR models with time‐varying transition probabilities

Jul 6, 2016