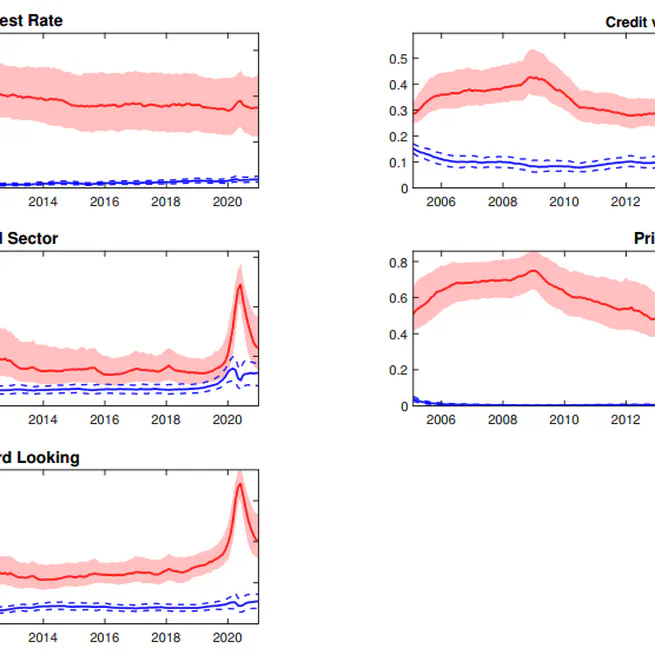

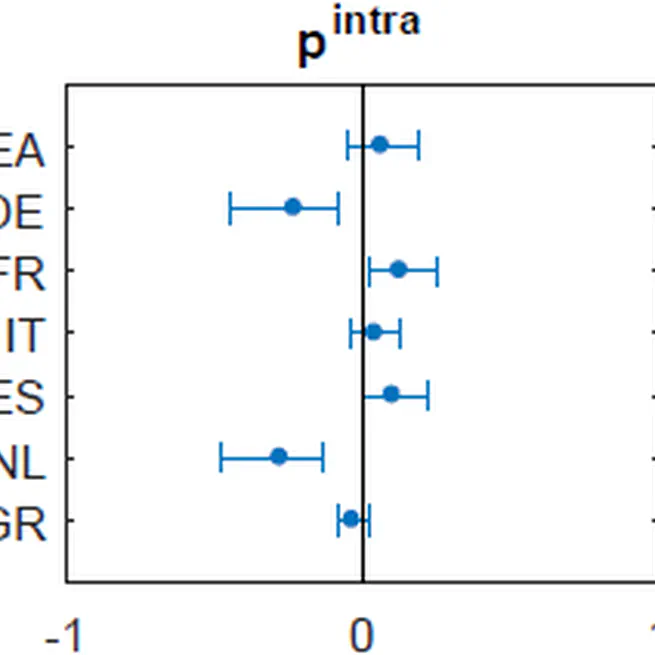

Financial integration or financial fragmentation? A euro area perspective

In this article we address the question of how strongly bank lending rates and credit volumes co-move across the euro area. Following the breakdown in the interest rate pass-through across the euro area, we aim to disentangle the relative importance of country-specific and common components in explaining the variance of the macro and financial variables by using a time-varying two-level dynamic factor model. Our results show that a high share is explained by the common component. However, we find a persistent decline in the importance of the common factor in the bank lending rates, indicating the presence of financial fragmentation. Furthermore, we find persistent heterogeneity across member states, specifically those hit hard by the sovereign-debt crisis.

May 13, 2022

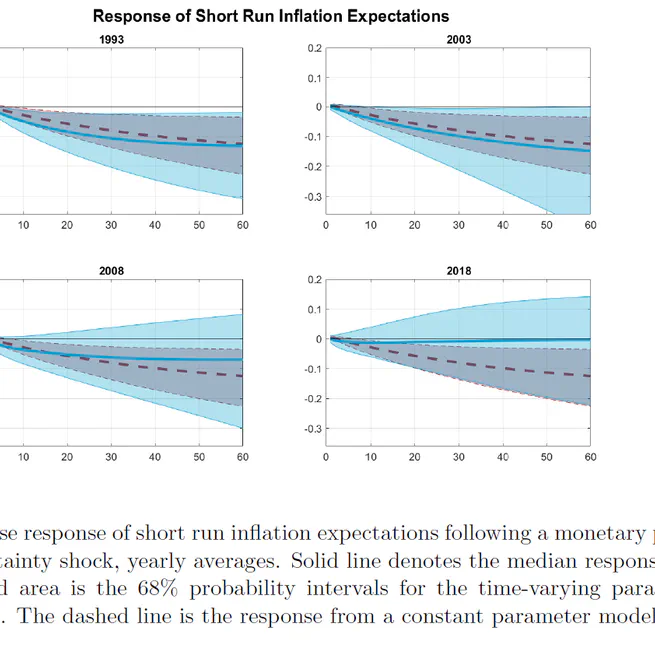

Monetary policy uncertainty and inflation expectations

In this paper we study whether inflation expectations in the U.S. react to changes in monetary policy uncertainty (MPU) as measured through the volatility of monetary policy shocks. We find that while they did, the importance of MPU has diminished and that it has different effects on short versus long-term inflation expectations.

Mar 1, 2021

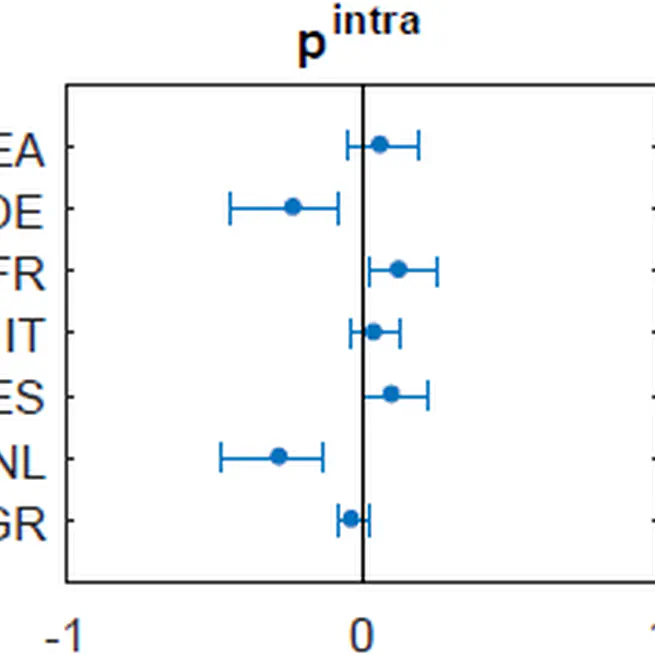

Exchange rate uncertainty and import prices in the euro area

This paper analyses the effects of exchange rate uncertainty on the pricing behaviour of import firms in the euro area. Uncertainty is measured via the volatility of the structural shocks to the exchange rate in a non-linear VAR framework and is an important determinant of import prices. An increase in exchange rate uncertainty is associated with a fall in prices on average, which suggests that the exchange rate risk is borne by the importers. The analysis utilizes a dataset on industrial import prices, disaggregated by origin of imports. Controlling for intra- and extra-euro area trade is important.

Aug 16, 2019

Financial crises and time-varying risk premia in a small open economy: a Markov-switching DSGE model for Estonia

May 2, 2018

The credibility of Hong Kong's currency board system: looking through the prism of MS‐VAR models with time‐varying transition probabilities

Jul 6, 2016